The healthcare logistics market is booming.

On July 15, healthcare logistics powerhouse Marken announced three acquisitions. Austria-based HETO, Hungary-based Der Kurier, and Italy-based HRTL all agreed to sell. Marken, in turn, was previously acquired by UPS, in an effort to create a life sciences supply chain leader.

The resulting company will cover 51 locations, 10 clinical storage depots, and worldwide reach. In addition, Marken will be able to deliver 7,000 clinical trial shipments every month.

Why is a parcel company pursuing a strategy in life sciences?

The answer is that UPS is just one of many companies that recognizes the opportunity in health care logistics. Also this year, we’ve seen a flurry of additional deals, including

- Pharmaceutical distribution leader McKesson’s acquisition of healthcare distributor Medical Specialties Distributors for $800 million

- Dental distribution giant Henry Schein’s acquisitions of Hayes Handpiece Franchises, Cliniclands, and Elite Computer Italia

- Healthcare distributor Cardinal Health’s acquisition of mscripts for SaaS-based mobile-based pharmacy solutions, along with its investment in the virtual hospital Medically Home Group

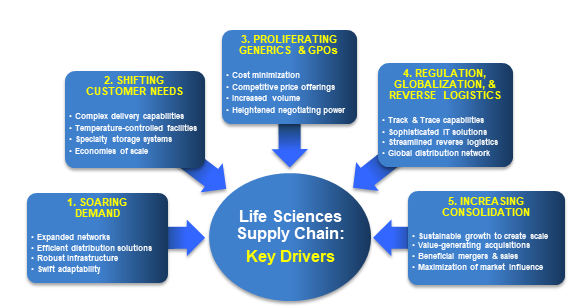

What are the root causes of driving change? I would highlight five core trends in particular: soaring demand, shifting customer needs, proliferating generics, regulation and reverse logistics, and consolidation. Each topic is outlined below.

Five trends driving change in life sciences logistics

-

Soaring Demand

As the world’s population ages, chronic diseases will become more common and increased pharmaceutical solutions will be necessary. In fact, the United Nations Department of Economic & Social Affairs estimates that the number of people over the age of 60 will nearly triple to about two billion by 2050 and will account for over 21 percent of the world population. In developed economies, the percentage of people over the age of 65 is already in the double digits and is expected to grow. Meanwhile, as the longevity of older persons in developing countries continues to rise, the need for pharmaceuticals in these countries will become amplified. Thus, the most predominant change in customer needs will come from a sheer increase in the volume of drugs and medical supplies demanded. In order to cement a piece of the expanding market, distributors will be tasked with widening their networks and investing in the infrastructure and technology to support them.

Drug shortages are also indicative of the changing marketplace. As chronic conditions become more prevalent, the need for medications that treat such diseases magnifies. Unfortunately, output tends not to keep pace with the growing need. In recent years, the use of injectable cancer treatments has increased by 20 percent without related production growth. Last year, there were over 100 reported disruptions in the supply of crucial medications. The conclusion: production will need to scale up, mounting further pressure on suppliers to provide efficient distribution solutions.

-

Shifting Customer Needs

As research and development continue to advance, drug portfolios of pharmaceutical firms will begin to take a different shape. By 2025, the global biologics market is expected to reach $400 billion. For pharmaceutical distributors, this translates into more complex means of manufacturing and delivery, such as the construction of additional climate-controlled facilities and specialty storage systems. Beyond new capital-intensive plants and equipment, we predict wholesalers who develop sufficient clout to play an active role in influencing which drugs will be dispensed most frequently will reap the largest profit from this trend.

Patients are also beginning to administer drugs in their homes. The global home healthcare market is estimated at $306 billion today, and is growing at 8% annually.

As a result, supply chains will have to learn to adapt to distributing to more locations, including residential homes, retirement homes and community centers. This was one catalyst for the Cardinal-Medically Home Group deal. Finding more economical ways to access local settings is key, and creating economies of scale is essential to ensure that numerous locations can be reached with ease.

-

Proliferating Generics and GPOs

Though changing customer needs are key components of the revolution in the pharmaceutical industry, evolving competitive dynamics are arguably an even greater piece of the transformation. The principal change the industry is experiencing is the fall from the “Generic Cliff” (the expiration of the patents of Big Pharma). As popular brand name drugs come off patent, companies will no longer be able to boost their bottom lines with brand name sales. Indeed, a recent government study found that on average, the retail price of a generic drug is 75 percent lower than its brand-name counterpart, with generics accounting for a staggering 78 percent of all drugs dispensed in retail settings. Consequently, companies are expected to look to their supply chains to find ways to streamline and cut costs.

Another competitive change will present itself as the Affordable Care Act takes effect. Pressure to provide the best care to an increasing number of patients with declining financial resources from public and private sector payers is resulting in an increased reliance on group purchasing organizations (GPOs) in order to cut costs. Already, about 72 percent of hospital purchases are made using GPO contracts. The specialized supply chains that these GPOs oversee are soon likely to experience increased activity, and the high-volume purchasing power GPOs leverage will place large companies who can offer competitive prices at a steep advantage. As a result, now more than ever it is critical for distributors to increase their volume to cut costs while boosting revenue.

-

Regulation, Globalization & Rise of Reverse Logistics

Companies must also be prepared to implement new federal regulations designed to protect the integrity of the pharmaceutical supply chain. Over the next 10 years, the FDA will phase in the Drug Supply Chain Security Act, which outlines specific “track and trace” requirements for wholesalers of prescription drugs. It also calls for a national electronic, interoperable system to identify and trace certain drugs as they are distributed. At the same time, the manufacturing and consumption of healthcare products in countries like Brazil, Russia, India and China (the BRICs) is resulting in a longer supply chain with increased costs and complexities. Indeed, the IMS forecasts China to experience 14 to 17% pharmaceutical sector growth annually, compared to 1–4% for the United States.

To ensure supply chain safety as regulation and globalization intensify, sophisticated technology solutions are in demand. Successful distributors have already begun to invest in state-of-the-art IT systems, such as advanced tracking and cloud computing, to more effectively exchange information, reduce fraud and exploit emerging markets.

Additionally, as oversight increases, recalls are more frequent and the removal of larger quantities of pharmaceuticals is required. The FDA recalled 4,448 drugs and device products last year. Expiration handling is also a growing market segment. Frequently, manufacturers insure the sale of particular drugs by guaranteeing to credit pharmacies for unsold product that reaches expiration. Combined with higher public scrutiny, an increased need for reverse logistics is emerging. And as globalization continues, instances of counterfeit drugs can be expected to multiply. The global market for fraudulent drugs is already estimated to be between $100-$200 billion a year, and the number of recorded cases of counterfeit, stolen or illegally diverted medicines has increased over 10x since 2002.

An opportunity thus presents itself for pharmaceutical distributors to position themselves as industry leaders by establishing and/or enhancing reverse logistics and supply chain security capabilities. This means developing additional sites and technological resources that will enable companies to take advantage of the high number of returns while safeguarding against counterfeits.

-

Increasing Consolidation

One final but critical market change is consolidation. We are witnessing a record level of healthcare M&A. In 2018, we saw 803 mergers and acquisitions, along with 858 affiliation and partnership announcements.

Industry analysts see this M&A wave continuing. Further, according to a Definitive Healthcare survey just released, industry consolidation was listed as the most important trend of the year, leading the way with 25.2% of the votes.

A key driver is the consolidation wave led by the Big Three in drug distribution, as mentioned above — Cardinal Health, McKesson, and AmerisourceBergen.

Astute companies in the life sciences supply chain are thus recognizing that value-generating mergers and acquisitions are a must. As distributors strive to achieve greater capacity, adapt to a market dominated by GPO-coordinated generic pharmaceutical purchases, and keep pace with escalating regulation and rapid globalization — all the while cutting costs and offering competitive prices — even more transactions are set to materialize in the next 12 months.

The Road Ahead: Challenge or Opportunity?

In light of the new burdens imposed on distributors by these five industry changes, we see three options available to companies in this sector:

- Establish critical capabilities through acquisitions, with a growth strategy to extend your network and enhance your competitive edge.

- Take advantage of favorable capital markets and record deal levels by pursuing a sale or utilizing additional equity to invest in the innovative technologies and modernized facilities necessitated by the transformation.

- Do nothing. However, consolidators like Medline, VWR, and others are swiftly pursuing acquisition-led growth, and you may find your competitive edge eroding in the face of more aggressive competitors.

To compete successfully, you should consider what strategies best allow you to cultivate a sustainable growth position in the evolving space. By contrast, unsuccessful companies will ignore the changing landscape at their peril. For companies stuck in between, you may find competitors gain economies of scale and long-term differentiation, while the majority in the middle will fall behind.

The life sciences supply chain sector faces an inflection point. While rising healthcare demand, proliferation of generic pharmaceuticals, and globalization can provide opportunities for medical distributors, intensifying competition, regulation, and consolidation pose sizeable challenges. Therefore, in light of fast-paced change, one thing is certain: as a buyer, a seller, or otherwise, now is a great time to solidify your strategy and take advantage of a favorable market.

What worries me is the inevitable shortage of drugs in the future. Also, until FDA gets stricter with its laws, the average medical cost is still too damn high. Anyways thats how its always been. Good job on the article though, it covers a lot of ground. And yea consolidation is the future for better and worse.

Hi Irshad,

Good points. The shortage of drugs will only increase the importance of cold chain logistics and technology!

-Benjamin Gordon